KLINEEGH 사기 피해 문의가 증가하고 있습니다. KLINEEGH 사기는 주식투자앱과 리딩방 구조를 결합해 출금 수수료 요구와 추가 입금 유도로 이어지는 특징이 확인됩니다.

업체명 : KLINEEGH

수법 : 투자 커뮤니티·SNS·오픈채팅 리딩방을 통해 무료 종목 정보와 내부 정보 기반 투자 기회를 미끼로 접근하고 투자 전문가·상담 담당자·고객센터 역할을 나눠 등장시키며 초기에는 수익이 발생한 것처럼 보여 신뢰 형성한 뒤 KLINEEGH 앱 설치와 플랫폼 가입을 유도하고 고수익 종목·VIP 투자·단기 급등 수익 등을 명목으로 투자 금액을 단계적으로 확대시키며 이후 출금 단계에서는 세금·출금 수수료·보증금·계좌 인증 등의 사유로 지급 지연시키고 선입금이 필요하다는 조건을 반복적으로 추가하며 추가 입금을 요구하는 방식으로 이어지는 구조

최근 KLINEEGH 사기 관련 피해 문의가

증가하는 흐름이 확인되고 있습니다.

KLINEEGH 사기는

무료 종목 정보와

가짜 투자앱 가입을 연결해

피해가 반복되는 구조로 보입니다.

초기에는 수익 화면을 보여주고

이후 출금 단계에서

세금, 수수료, 보증금 명목으로

추가 입금을 요구하는 흐름이

확인됩니다.

이번 글에서는

접근 방식, 앱 설치 유도,

출금 지연 구조,

대응 전 확인해야 할 자료를

순서대로 정리합니다.

목차

- 리딩방 유입과 초기 신뢰 형성 구조

- 가짜 주식투자앱 설치와 플랫폼 가입 유도

- 출금 수수료 요구와 추가 입금 패턴

- 피해자가 확인해야 할 위험 신호

- 대응 전 정리해야 할 자료와 방향

1. KLINEEGH 사기 유입은 리딩방 신뢰 형성에서 시작됩니다

처음 접근은

대부분 직접적인 투자 요구보다

무료 정보 제공으로 시작됩니다.

투자 커뮤니티, SNS 광고,

오픈채팅 리딩방을 통해

“무료 종목 정보”

“내부 정보 기반 투자”

“단기 급등 가능 종목” 같은 문구가

제시되는 방식입니다.

무료 종목 정보로 경계심을 낮추는 단계

초기에는 돈을 요구하지 않습니다.

오히려 시장 분석 자료와

종목 추천 내용을 제공하며

상대방이 스스로 신뢰하도록

분위기를 만듭니다.

이때 리딩방 안에서는

다른 참여자들이 수익 인증을 올리거나

전문가의 추천이 맞았다는 식의

대화가 반복될 수 있습니다.

피해자는 이를 보며

정상 투자 커뮤니티라고

오해하기 쉽습니다.

“초기 무료 정보는 피해자의 경계심을 낮추기 위한 신뢰 장치로 활용되는 경우가 많습니다.”

전문가·상담 담당자·고객센터 역할 분리

이 유형에서는

한 명만 등장하지 않는 경우가 많습니다.

투자 전문가는 종목을 설명하고,

상담 담당자는 가입을 안내하며,

고객센터는 입금과 출금 절차를

담당하는 것처럼 행동합니다.

역할이 나뉘면

피해자는 실제 회사 조직처럼

느낄 가능성이 커집니다.

그러나 이 구조는

책임을 분산시키고

피해자의 판단을 흐리게 만드는

장치로 사용될 수 있습니다.

실제 피해 흐름 예시

한 피해자는

SNS 광고를 통해

무료 종목방에 들어갔습니다.

처음 며칠 동안은

종목 정보와 매매 타이밍만 제공됐고

리딩방 안에서는 수익 인증이

계속 올라왔습니다.

이후 상담 담당자가

더 높은 수익을 위해서는

전용 앱 가입이 필요하다고 안내했습니다.

소액 투자 후

수익이 표시되자 신뢰가 생겼고

투자 금액은 점차 커졌습니다.

하지만 출금을 요청하자

수수료와 계좌 인증비가 필요하다는

조건이 추가되었습니다.

결국 피해자는

출금을 위해 다시 입금해야 한다는

압박을 받게 되었습니다.

2. 가짜 주식투자앱 설치와 플랫폼 가입 유도

이 유형의 핵심은

리딩방에서 끝나지 않고

별도 앱 설치로 이어진다는 점입니다.

겉으로는 주식투자앱처럼 보이지만

실제 거래가 정상 시장과 연결되는지

확인하기 어려운 구조가 많습니다.

KLINEEGH 앱 설치 유도 방식

운영자는

“전용 투자 시스템”

“VIP 회원 전용 앱”

“고수익 종목 참여 플랫폼”이라는

표현을 사용합니다.

피해자는

일반 증권사 앱처럼 생각하고

가입을 진행할 수 있습니다.

하지만 설치 경로가 불명확하거나

공식 마켓이 아닌 외부 링크를 통해

앱 설치를 요구한다면

주의가 필요합니다.

정상적인 금융 거래 플랫폼은

사업자 정보, 서비스 구조,

고객 보호 절차가 명확해야 합니다.

수익 화면으로 신뢰를 강화하는 방식

앱에 가입한 뒤에는

잔고와 수익률이 표시됩니다.

초기에는

소액 투자에서 수익이 난 것처럼

화면이 구성될 수 있습니다.

일부 사례에서는

소액 출금이 가능했던 것처럼

보이는 흐름도 나타납니다.

이 단계가 위험한 이유는

피해자가 “정상적으로 작동한다”고

믿게 된다는 점입니다.

이후 운영자는

더 큰 투자 기회를 제시하며

금액 확대를 유도합니다.

“수익 화면이 보인다는 사실만으로 실제 거래가 이루어졌다고 단정할 수 없습니다.”

VIP 투자와 단기 급등 수익 명목

신뢰가 형성되면

VIP 투자 참여가 제안됩니다.

운영자는

“이번 종목은 단기 급등 가능성이 높다”

“내부 정보가 확인됐다”

“일반 회원은 참여할 수 없다”는 식으로

희소성을 강조합니다.

이런 표현은

피해자가 빠르게 결정하도록

압박하는 요소가 됩니다.

특히 이미 일부 수익을 봤다고 느낀 상태라면

추가 입금 결정이 쉬워질 수 있습니다.

실제 피해 흐름 예시

한 사례에서는

오픈채팅방에서 전문가가

무료 종목을 추천했습니다.

며칠 뒤 상담 담당자가

KLINEEGH 앱 설치를 안내했고

피해자는 안내에 따라 가입했습니다.

처음에는

소액 투자 수익이 표시됐고

리딩방 안에서도 비슷한 수익 인증이

반복적으로 올라왔습니다.

이후 VIP 종목 참여를 권유받아

투자금이 커졌습니다.

하지만 출금을 신청하자

세금과 보증금이 필요하다는

안내가 이어졌습니다.

입금을 마친 뒤에도

추가 인증비가 필요하다는

새 조건이 다시 발생했습니다.

3. 출금 수수료 요구와 추가 입금 패턴

KLINEEGH 사기에서

피해가 본격적으로 드러나는 구간은

출금 단계입니다.

수익이 표시되는 것과

실제로 돈을 돌려받는 것은

전혀 다른 문제입니다.

출금 요청 후 조건이 바뀌는 구조

피해자가 출금을 요청하면

운영자는 여러 사유를 제시합니다.

대표적으로

세금, 출금 수수료,

보증금, 계좌 인증,

보안 검수 등이 언급됩니다.

문제는

이 조건이 한 번으로 끝나지 않는다는 점입니다.

하나를 납부하면

다른 조건이 추가되고,

다시 입금하면

또 다른 이유로 출금이 미뤄지는

흐름이 반복됩니다.

“출금 단계에서 선입금 조건이 반복된다면 구조 자체를 의심해야 합니다.”

선입금 요구가 위험한 이유

정상적인 투자 서비스라면

출금할 금액에서 비용을 공제하거나

명확한 약관과 절차를 안내해야 합니다.

그러나 사칭 플랫폼에서는

출금을 해주기 전

먼저 돈을 보내야 한다고 말합니다.

이때 피해자는

이미 큰 금액이 묶여 있기 때문에

추가 입금을 고민하게 됩니다.

“이번만 내면 출금된다”는 말이

가장 위험한 압박 문구가 될 수 있습니다.

단계별 구조 정리

| 단계 | 설명 | 특징 |

|---|---|---|

| 1단계 | 초기 접촉 | SNS, 커뮤니티, 오픈채팅 유입 |

| 2단계 | 신뢰 형성 | 무료 종목 정보와 수익 인증 |

| 3단계 | 투자 진행 | 앱 설치와 플랫폼 가입 유도 |

| 4단계 | 금액 확대 | VIP 투자와 고수익 종목 강조 |

| 5단계 | 출금 제한 | 세금, 수수료, 보증금 요구 |

| 6단계 | 추가 입금 | 조건 반복 변경 |

실제 피해 흐름 예시

피해자는

커뮤니티에서 무료 종목 정보를 보고

리딩방에 참여했습니다.

초기에는

전문가가 추천한 종목에서

수익이 발생한 것처럼 보였습니다.

이후 전용 플랫폼 가입 후

투자 금액을 늘렸고

잔고 화면에는 수익이 계속 표시됐습니다.

하지만 출금을 요청하자

고객센터는 세금 납부가 필요하다고 했습니다.

세금을 입금하자

이번에는 출금 수수료가 필요하다고 했고,

다시 입금한 뒤에는

계좌 인증 보증금이 필요하다는

안내가 이어졌습니다.

결국 출금은 진행되지 않았고

추가 입금 요구만 반복되었습니다.

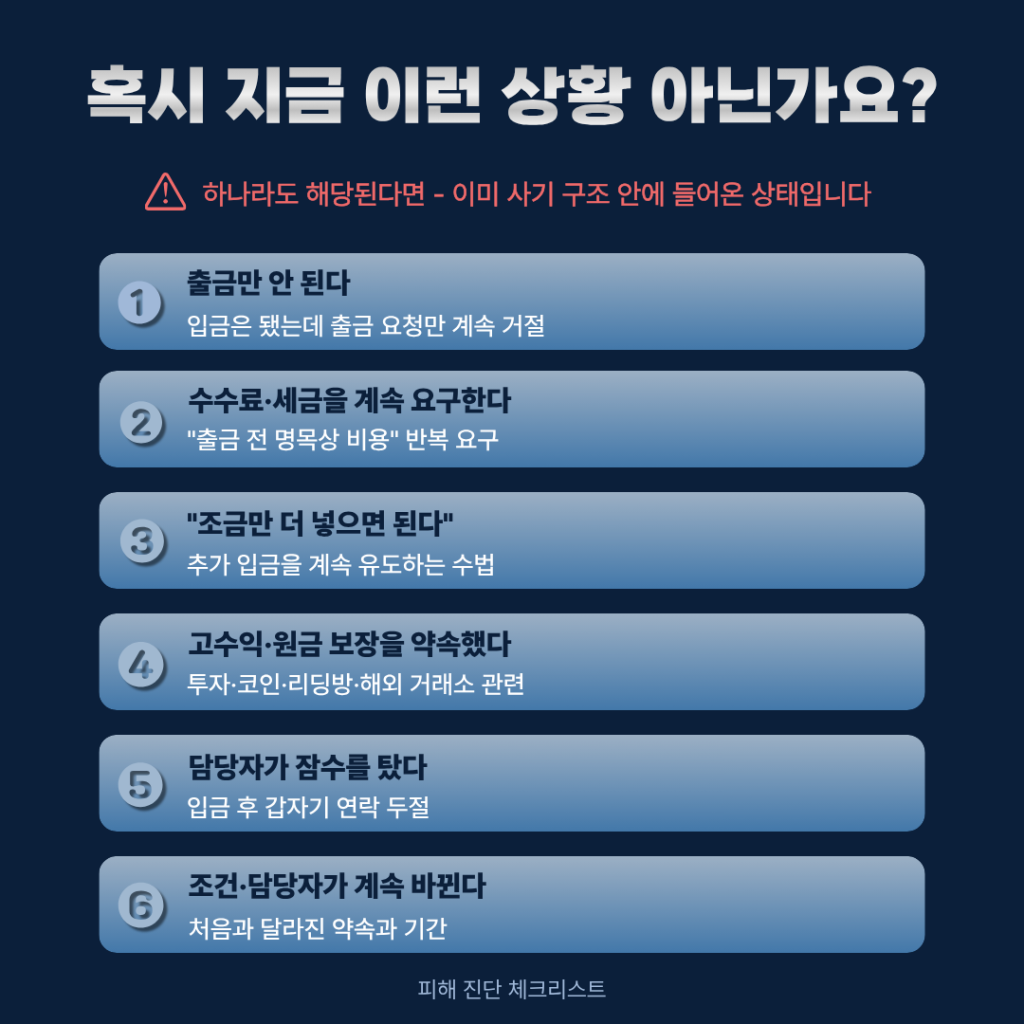

4. 피해자가 확인해야 할 위험 신호

이 유형은

처음부터 명확히 드러나지 않는 경우가 많습니다.

겉으로는

투자 정보방,

전문가 리딩,

주식투자앱 서비스처럼 보이기 때문입니다.

지나치게 높은 수익률 강조

단기간 고수익,

확정 수익,

급등 예정 종목이라는 표현은

주의 깊게 봐야 합니다.

정상적인 투자에서는

수익을 보장할 수 없습니다.

그럼에도 운영자가

“이번 기회는 확실하다”

“내부 정보라 안전하다”

“VIP만 참여 가능하다”고 말한다면

위험 신호로 볼 수 있습니다.

특히 리딩방 안에서

동일한 수익 인증이 반복된다면

연출된 분위기일 가능성도 고려해야 합니다.

출금 전 선입금 요구

가장 중요한 판단 기준은

출금 단계입니다.

수익이 표시되는 것보다

실제 출금이 되는지가 중요합니다.

출금 전

세금, 수수료, 보증금,

계좌 인증비를 먼저 보내라고 한다면

추가 피해로 이어질 수 있습니다.

특히

“오늘 처리하지 않으면 계정이 정지된다”

“마지막 단계다”

“기한 내 납부해야 한다”는 식의

압박이 동반되면 더욱 주의해야 합니다.

“수익 화면보다 중요한 것은 실제 출금 가능 여부입니다.”

고객센터가 입금을 압박하는 상황

정상 고객센터라면

문제를 해결하기 위한

객관적 절차를 안내해야 합니다.

그러나 사칭 플랫폼의 고객센터는

문제 해결보다 입금을 요구하는 경우가 많습니다.

출금이 안 되는 이유가

계속 바뀌고,

담당자가 바뀌며,

답변이 지연된다면

구조를 다시 확인해야 합니다.

또한 채팅방 삭제,

계정 차단,

앱 접속 제한이 함께 나타난다면

자료 확보가 우선입니다.

실제 피해 흐름 예시

한 피해자는

처음에는 무료 종목 리딩만 받았습니다.

이후 전문가가

단기 급등 종목을 알려준다며

앱 가입을 권유했습니다.

피해자는

초기 수익 화면을 보고

정상 투자라고 판단했습니다.

하지만 출금 요청 이후

고객센터는

계좌 인증비를 요구했습니다.

이후 보증금, 세금,

수수료 명목이 추가되며

입금 요구가 반복됐습니다.

마지막에는

리딩방과 고객센터 모두

응답이 늦어졌고

일부 대화 내용이 삭제되었습니다.

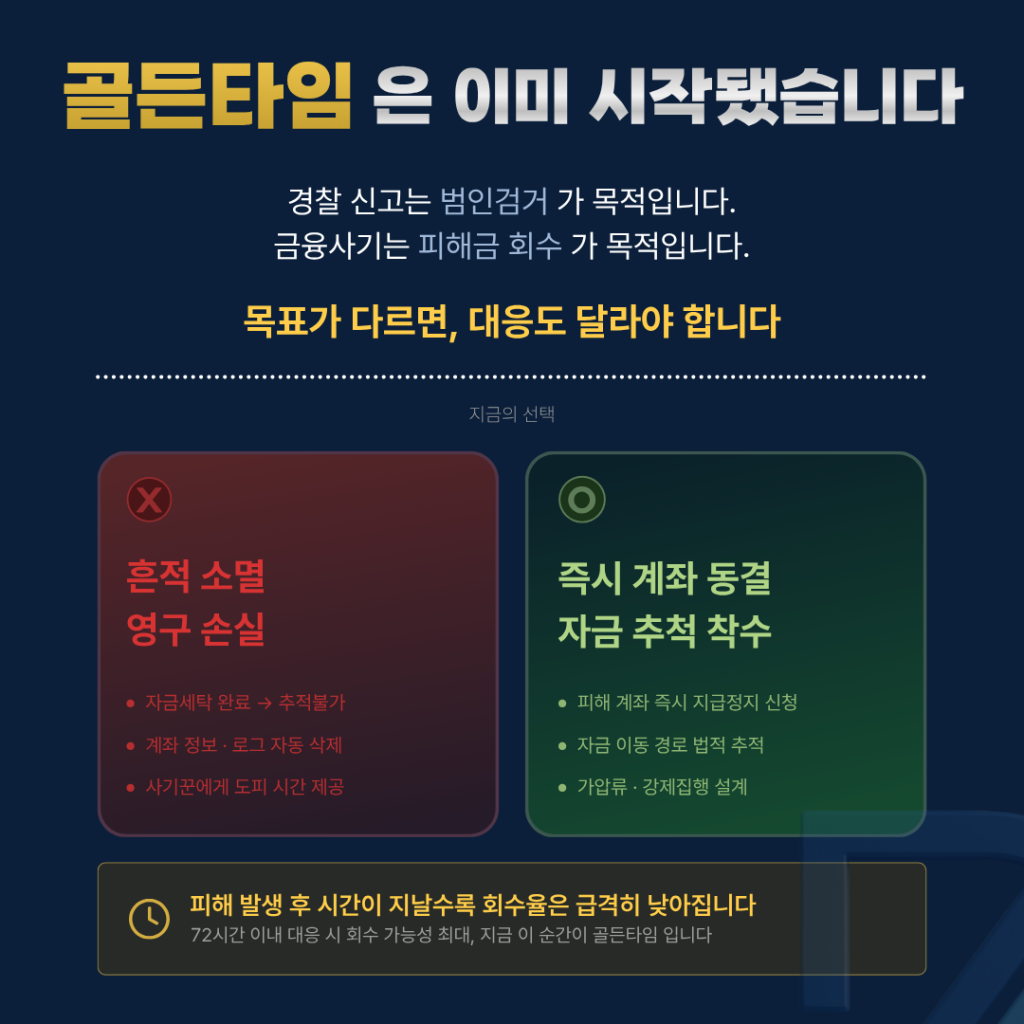

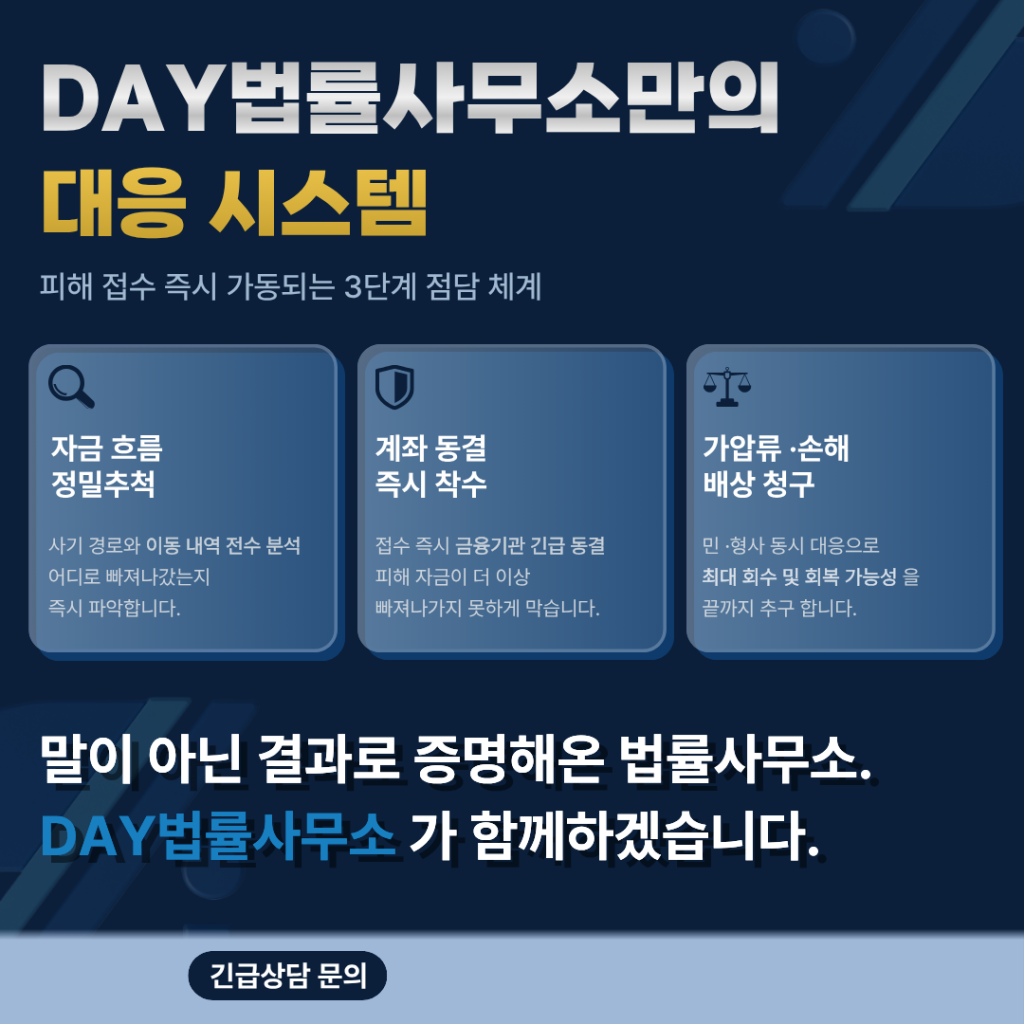

5. 대응 전 정리해야 할 자료와 방향

KLINEEGH 사기 의심 상황에서는

감정적으로 대응하기보다

자료를 먼저 정리하는 것이 중요합니다.

시간이 지나면

채팅방이 사라지거나

앱 접속이 막힐 수 있기 때문입니다.

반드시 확보해야 할 자료

우선 대화 기록을 저장해야 합니다.

리딩방 안내 내용,

전문가 발언,

상담 담당자 대화,

고객센터 답변을

순서대로 정리하는 것이 좋습니다.

입금 내역도 중요합니다.

입금 계좌,

입금 시간,

입금 금액,

입금 명목을 구분해 두어야 합니다.

앱 화면도 저장해야 합니다.

잔고 화면,

수익률 화면,

출금 신청 화면,

오류 메시지,

수수료 요구 화면이 포함됩니다.

추가 입금 중단 필요성

출금이 지연된 상태에서

추가 입금을 요구받고 있다면

먼저 멈추고 구조를 확인해야 합니다.

운영자는

출금을 위해 반드시 필요하다고

설명할 수 있습니다.

하지만 이미 납부한 뒤에도

조건이 반복된다면

동일한 방식이 계속될 가능성이 있습니다.

추가 입금은 피해 규모를 키우는

가장 직접적인 요인이 될 수 있습니다.

자료 정리 표

| 구분 | 확인 자료 | 정리 이유 |

|---|---|---|

| 대화 기록 | 리딩방, 상담자, 고객센터 대화 | 접근과 유도 흐름 확인 |

| 입금 내역 | 계좌, 금액, 시간, 명목 | 자금 이동 경로 확인 |

| 앱 화면 | 잔고, 수익률, 출금 신청 | 허위 표시 구조 확인 |

| 요구 명목 | 세금, 수수료, 보증금 | 추가 입금 패턴 확인 |

| 접속 정보 | 링크, 앱 주소, 계정 정보 | 플랫폼 실체 확인 |

실제 대응 전 확인할 부분

피해 상황을 정리할 때는

단순히 총 피해금만 보는 것이 아니라

어떤 순서로 돈을 보냈는지가 중요합니다.

접근 경로,

신뢰 형성 과정,

투자 금액 확대 시점,

출금 지연 사유,

추가 입금 요구 내용을

시간순으로 정리해야 합니다.

유사한 구조는

다른 리딩방 사기와

가짜거래소 사례에서도

반복적으로 확인됩니다.

외부 참고 자료와

유사 사례 분석 글을 함께 보면

현재 상황을 객관적으로 판단하는 데

도움이 될 수 있습니다.

“피해 대응의 시작은 감정적 설득이 아니라 기록의 정리입니다.”

결론

KLINEEGH 사기 의심 사례는

무료 종목 정보와 리딩방 신뢰 형성을 거쳐

가짜 주식투자앱 설치로 이어지는

구조적 특징이 있습니다.

특히 출금 단계에서

세금, 수수료, 보증금,

계좌 인증 명목이 반복된다면

주의가 필요합니다.

수익 화면이 보인다는 이유만으로

정상 거래라고 단정해서는 안 됩니다.

현재 필요한 것은

추가 입금 여부를 멈추고

대화 기록과 입금 내역을

정확히 정리하는 것입니다.

피해 흐름을 시간순으로 정리해야

이후 대응 방향을 판단하는 데

도움이 될 수 있습니다.

English Version

Fake Investment App Fraud Warning: Key Patterns Behind the KLINEEGH-Type Scheme

Recently, fake investment app cases connected to stock advisory chat rooms have continued to appear in various online communities.

These cases often begin with what appears to be harmless investment information.

Victims are invited through social media advertisements, investment communities, or open chat groups.

At first, the operators usually do not demand a large deposit.

Instead, they provide free stock information, market commentary, and screenshots showing successful profits.

This process is designed to reduce suspicion and make the victim believe that the group is operated by experienced investment professionals.

The structure then moves from a chat-based advisory environment into a separate investment platform.

Once the victim installs the app and joins the platform, the operators begin encouraging larger deposits through high-profit stock recommendations, VIP investment opportunities, and short-term trading events.

The most serious problem usually appears when the victim attempts to withdraw funds.

At that stage, the platform may introduce taxes, withdrawal fees, deposits, account verification charges, or other advance payment conditions.

The key feature of this structure is that the conditions often do not end after one payment.

A new reason may appear, and the victim may be pressured to send more money.

1. How the Initial Contact Is Designed

The first stage usually begins with a low-pressure invitation.

The victim may see a social media advertisement, join an investment community, or receive an invitation to an open chat room.

The message often promotes free stock information, special market insight, or exclusive opportunities based on internal information.

At this point, the operator does not immediately ask for a large amount of money.

Instead, the group creates an environment that looks active and professional.

Several accounts may post messages claiming that they earned profits from the recommended stocks.

Others may thank the expert or say that the guidance was accurate.

This kind of repeated social proof can make the victim believe that the group is legitimate.

“In many fake investment structures, trust is built before money is requested.”

The victim may then begin following the group more closely.

They may receive market updates, recommended entry points, and explanations about short-term price movements.

The more consistent the communication appears, the easier it becomes for the victim to lower their guard.

This early stage is not just information sharing.

It is often the foundation for later financial pressure.

2. Role Separation Inside the Operation

A notable feature of this type of fraud is role separation.

One person may appear as an investment expert.

Another may act as a consultation manager.

A third person may present themselves as a customer service representative.

This creates the impression of a real organization.

The investment expert explains the market.

The consultation manager guides account registration.

The customer service representative handles deposit and withdrawal questions.

To the victim, this may seem structured and professional.

However, this role separation can also make it difficult to identify who is responsible.

When a problem occurs, one person may claim that another department is handling the matter.

This delays the victim’s response and keeps the victim inside the system for a longer period.

In many reported cases, the victim continues communicating with multiple operators even after withdrawal restrictions appear.

3. The Fake Investment App Stage

After trust has been established, the victim is often guided to install a separate investment app.

The app may be described as a VIP-only system, a professional trading platform, or an exclusive stock investment service.

The operator may say that normal members cannot access the same opportunities.

This creates a sense of scarcity.

The victim may believe that they are receiving special access.

Once inside the platform, the screen may display account balances, profit rates, trade histories, and pending withdrawals.

These screens can look convincing.

However, a displayed profit number does not prove that real trading has occurred.

In fake platform cases, the balance screen may simply be controlled by the operators.

This is why victims should not judge legitimacy based only on the app interface.

“A visible balance does not guarantee that the funds are actually available for withdrawal.”

4. Small Profit Experience and Trust Expansion

Some victims report that the platform initially shows successful profits.

In certain cases, a small withdrawal may appear to work.

This stage is especially dangerous.

A small successful withdrawal can make the victim believe that the system is real.

After that, the operator may recommend a larger opportunity.

The message may include phrases such as:

- VIP trading event

- High-profit stock opportunity

- Short-term surge stock

- Internal information strategy

- Limited participation window

These phrases are designed to create urgency.

The victim may feel that they will miss an important opportunity if they hesitate.

As the investment amount increases, the victim becomes more emotionally and financially tied to the platform.

This makes it harder to stop even when warning signs begin to appear.

5. Withdrawal Restrictions and Advance Payment Demands

The withdrawal stage is where many victims realize that something is wrong.

The app may still display profits.

The account balance may still look positive.

However, when the victim attempts to withdraw, the platform introduces new requirements.

Common reasons include:

- Tax payment

- Withdrawal processing fee

- Security deposit

- Account verification

- Bank account review

- Compliance check

The operator may say that the withdrawal cannot be processed unless the victim pays first.

After one payment is made, another condition may be introduced.

This repeated condition-setting is a major warning sign.

A legitimate financial service should have clear rules and transparent procedures.

It should not repeatedly create new advance payment requirements whenever a withdrawal is requested.

6. Why Victims Continue Sending Money

Many victims continue sending money because they believe the withdrawal is almost complete.

The operators often use phrases such as:

- This is the final step

- The withdrawal is already approved

- Only the verification fee remains

- The account will be released after this payment

- Delay may cause account suspension

These phrases create pressure.

The victim is not only trying to earn profit.

They are trying to recover money that has already been deposited.

This recovery pressure is one of the strongest psychological tools used in these schemes.

The larger the existing deposit, the harder it becomes for the victim to refuse another payment.

The victim may think, “I have already sent so much. I need to complete one more step.”

This is exactly the point where the damage can expand further.

7. Common Warning Signs

There are several warning signs that should be reviewed carefully.

First, the investment opportunity is introduced through an informal channel such as an open chat group or social media message.

Second, the group repeatedly shows profit screenshots without verifiable evidence.

Third, the operator asks the victim to install a separate app through an unclear route.

Fourth, the platform displays profits but blocks withdrawals.

Fifth, the customer service team demands taxes, fees, deposits, or verification payments before processing withdrawals.

Sixth, the reason for the delay changes repeatedly.

Seventh, the operators pressure the victim to act quickly.

When several of these signs appear together, the situation should be reviewed carefully before sending additional funds.

8. Evidence That Should Be Preserved

When a victim suspects a fake investment platform, preserving evidence becomes important.

The first category is communication records.

This includes chat room messages, private conversations, expert recommendations, consultation guidance, and customer service replies.

The second category is payment records.

The victim should organize bank transfer details, dates, amounts, account names, and payment reasons.

The third category is platform evidence.

Screenshots of the app interface, account balance, profit screen, withdrawal request, error messages, and fee demands may all be relevant.

The fourth category is access information.

This includes platform links, app download paths, account IDs, and any contact information used by the operators.

Evidence should be saved before deleting the app or leaving the chat room.

In many cases, access may suddenly be blocked after the victim asks too many questions.

9. Why Additional Deposits Should Be Reviewed Carefully

When withdrawal is delayed, the operator may insist that an additional payment is required.

This is the most critical moment.

The victim may feel that paying once more is the only way to recover the full amount.

However, if previous payments did not result in withdrawal, another payment may simply extend the same pattern.

The victim should review whether the condition is clear, whether it is supported by real documentation, and whether the platform has already changed its explanation multiple times.

If the reason keeps changing, the structure itself may be the problem.

At that point, the priority should shift from paying more money to organizing records and analyzing the full transaction flow.

10. Final Summary

This type of fake investment app structure often follows a repeated pattern.

The victim is approached through a community, social media, or an open chat room.

Trust is created through free stock information and profit screenshots.

The victim is then guided to install a separate platform.

The displayed profits encourage larger deposits.

When the victim requests withdrawal, new conditions appear.

Taxes, fees, deposits, or account verification payments may be demanded in advance.

The most important issue is not whether the app shows profit.

The real question is whether the funds can actually be withdrawn without new conditions being added.

When withdrawal delays and repeated advance payment demands appear together, the situation should be reviewed carefully.

The safest first step is to stop additional deposits, preserve records, and organize the full sequence of contact, trust-building, deposit, withdrawal delay, and further payment demands.

#KLINEEGH사기

#주식투자앱

#리딩방사기

#출금수수료요구

#가짜거래소사기

#허위플랫폼사기

#투자사기

#출금불가